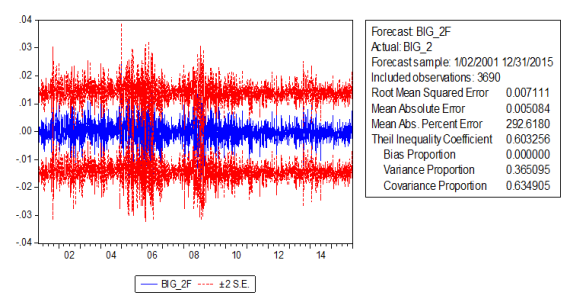

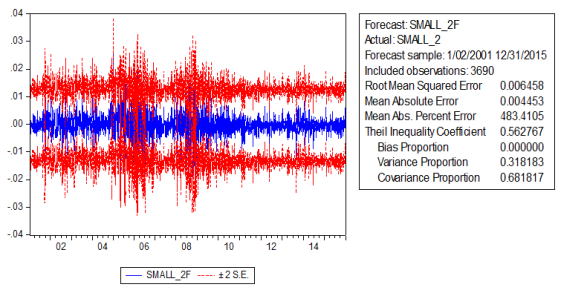

This study aims to forecast asset variances and covariances through the application of multi-scale risk models. Using daily data for 61 firms listed on the Amman Stock Exchange (ASE) over the period from January 1, 2001, to December 31, 2015, the analysis investigates the dynamic behaviour of asset returns across different time horizons. To enhance the robustness and reliability of the findings, several econometric and statistical techniques are employed, including the CUSUM test to assess structural stability, the Granger causality test to examine predictive relationships, wavelet transformation to capture time-frequency dynamics, and unit root tests to verify stationarity properties. The multi-scale risk model serves as the principal analytical framework, allowing for a comprehensive examination of the evolving interdependencies among asset returns. The empirical results indicate that market risk premium coefficients significantly explain variations in portfolio returns, highlighting the importance of systematic risk factors in asset pricing. Furthermore, portfolios composed of lower-value stocks outperform those containing higher-value stocks, while smaller-sized portfolios consistently generate higher returns than larger-sized portfolios during the sample period. Overall, the findings demonstrate the effectiveness of multi-scale risk models in forecasting asset variances and covariances. The model exhibits strong explanatory power in capturing daily portfolio return dynamics on the ASE, thereby contributing to improved portfolio optimization strategies and more accurate risk prediction. These results underscore the practical and theoretical value of multi-scale modelling in financial risk management.

| Published in | Journal of Business and Economic Development (Volume 11, Issue 1) |

| DOI | 10.11648/j.jbed.20261101.11 |

| Page(s) | 1-15 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2026. Published by Science Publishing Group |

Forecasting, Portfolio Variances and Covariances, Multi-scale Risk Models, Market Risk Premium, Wavelet Transform, Granger Causality Test, Unit Root Tests, Amman Stock Exchange (ASE)

Item | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 |

|---|---|---|---|---|---|---|---|---|---|---|---|

Number of Listed Companies | 201 | 227 | 245 | 262 | 272 | 277 | 247 | 243 | 240 | 236 | 228 |

No. of Trading Days | 244 | 242 | 247 | 245 | 249 | 250 | 247 | 251 | 245 | 249 | 246 |

Turnover Ratio (%) | 94.1 | 101.1 | 91.2 | 91.5 | 91.3 | 102.2 | 58.2 | 33.9 | 38 | 32.8 | 37.3 |

ASE General Free Float Weighted Price Index (point) | 4259.7 | 3013.7 | 3675 | 2758.4 | 2533.5 | 2373.6 | 1995.1 | 1957.6 | 2065.8 | 2165.5 | 2136.3 |

P/E Ratio (times) | 44.2 | 16.7 | 28 | 18.8 | 14.4 | 26.3 | 22.6 | 15.6 | 14.7 | 15.3 | 14 |

P/BV (times) | 3.2 | 2.9 | 3 | 2.2 | 1.8 | 1.7 | 1.5 | 1.5 | 1.3 | 1.3 | 1.3 |

Dividend Yield Ratio (%) | 1.6 | 2.3 | 1.8 | 2.5 | 2.8 | 2.7 | 3.3 | 4.6 | 4.6 | 4.2 | 3.6 |

Non-Jordanian Buying (JD million) | 2,152.20 | 1,995.10 | 2,825.30 | 4,219.80 | 2,135.50 | 1,036.60 | 555.8 | 322.9 | 939.5 | 362.7 | 981.7 |

Non-Jordanian Selling (JD million) | 1739.2 | 1814.5 | 2359.1 | 3910 | 2139.3 | 1051.2 | 477.2 | 285.3 | 792.6 | 384.8 | 971.1 |

Market Capitalization / GDP (%) | 326.6 | 233.9 | 289 | 216.7 | 149.6 | 122.7 | 102.7 | 93.5 | 83 | 75.8 | 70.7 |

Variable | Obs. | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

Rm-Rf | 3690 | 0.01% | 0.91% | -4.56% | 5.99% |

HML | 3690 | 0.02% | 0.81% | -9.00% | 7.40% |

SMB | 3690 | 0.02% | 1.08% | -8.60% | 13.60% |

Big | 3690 | 0.02% | 1.00% | -21.50% | 11.80% |

Big 1 | 3690 | 0.03% | 0.89% | -7.00% | 5.50% |

Big 2 | 3690 | 0.03% | 0.80% | -5.80% | 12.30% |

Small | 3690 | 0.03% | 1.06% | -13.60% | 6.90% |

Small 1 | 3690 | 0.03% | 0.91% | -7.00% | 4.50% |

Small 2 | 3690 | 0.04% | 0.75% | -9.80% | 3.20% |

High | 3690 | 0.03% | 0.96% | -8.90% | 11.00% |

High 1 | 3690 | 0.03% | 0.88% | -19.60% | 10.80% |

High 2 | 3690 | 0.02% | 0.81% | -15.40% | 7.80% |

Low | 3690 | 0.04% | 1.03% | -14.60% | 12.40% |

Low 1 | 3690 | 0.04% | 0.95% | -12.50% | 5.40% |

Low 2 | 3690 | 0.02% | 0.82% | -8.00% | 3.80% |

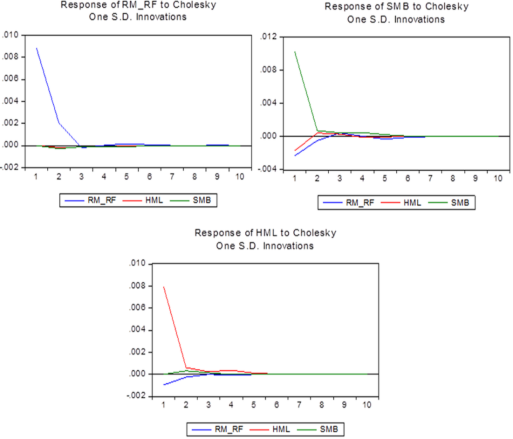

HML | RM_RF | SMB | |

|---|---|---|---|

Correlation Matrix for the Explanatory Variables | |||

HML | 1 | ||

RM_RF | -0.12750 | 1 | |

SMB | -0.12206 | -0.22674 | 1 |

Residual Correlation Matrix | |||

HML | 1 | ||

RM_RF | -0.12044 | 1 | |

SMB | -0.13367 | -0.21802 | 1 |

Covariance Matrix of the Residuals | |||

HML | 0.00006 | -0.00001 | -0.00001 |

RM_RF | -0.00001 | 0.00008 | -0.00002 |

SMB | -0.00001 | -0.00002 | 0.00011 |

Null Hypothesis: | Obs. | F-Statistic | Prob. |

|---|---|---|---|

HML does not Granger Cause SMB | 3689 | 13.7815*** | 0.000 |

SMB does not Granger Cause HML | 8.45492*** | 0.004 | |

RM_RF does not Granger Cause SMB | 3689 | 1.55186 | 0.213 |

SMB does not Granger Cause RM_RF | 3.26094* | 0.071 | |

RM_RF does not Granger Cause HML | 3689 | 1.79888 | 0.180 |

HML does not Granger Cause RM_RF | 1.94782 | 0.163 |

Test Critical Values: | T-Statistic | Prob.* | |||

|---|---|---|---|---|---|

1% level | 5% level | 10% level | |||

SMB | -3.432 | -2.862 | -2.567 | -56.314*** | 0.000 |

HML | -3.432 | -2.862 | -2.567 | -55.756*** | 0.000 |

RM_RF | -3.432 | -2.862 | -2.567 | -41.045*** | 0.000 |

SMALL | -3.432 | -2.862 | -2.567 | -49.736*** | 0.000 |

SMALL 1 | -3.432 | -2.862 | -2.567 | -53.509*** | 0.000 |

SMALL 2 | -3.432 | -2.862 | -2.567 | -55.154*** | 0.000 |

BIG | -3.432 | -2.862 | -2.567 | -55.447*** | 0.000 |

BIG 1 | -3.432 | -2.862 | -2.567 | -54.054*** | 0.000 |

BIG 2 | -3.432 | -2.862 | -2.567 | -53.903*** | 0.000 |

LOW | -3.432 | -2.862 | -2.567 | -53.027*** | 0.000 |

LOW 1 | -3.432 | -2.862 | -2.567 | -53.280*** | 0.000 |

LOW 2 | -3.432 | -2.862 | -2.567 | -52.316*** | 0.000 |

HIGH | -3.432 | -2.862 | -2.567 | -51.617*** | 0.000 |

HIGH1 | -3.432 | -2.862 | -2.567 | -55.411*** | 0.000 |

HIGH2 | -3.432 | -2.862 | -2.567 | -56.690*** | 0.000 |

Portfolios | αi | βMRP | βHML | βSMB | t(αi) | t(βMRP) | t(βHML) | t(βSMB) | Adjusted R2 | F-Ratio | D-W stat. |

|---|---|---|---|---|---|---|---|---|---|---|---|

SMALL | -0.0002* | 0.847*** | -0.241*** | -0.185*** | -1.78 | 77.31 | -19.82 | -20.04 | 69.4% | 2793.93 | 1.987 |

SMALL 1 | -0.0002** | 0.667*** | -0.070*** | -0.104*** | -2.21 | 55.37 | -5.23 | -10.25 | 50.7% | 1267.28 | 2.004 |

SMALL 2 | -0.0003*** | 0.425*** | -0.026* | 0.001 | -3.11 | 35.01 | -1.93 | 0.14 | 26.7% | 448.78 | 1.913 |

BIG 2 | -0.0003** | 0.423*** | 0.018 | 0.088*** | -2.24 | 31.66 | 1.25 | 7.77 | 21.6% | 339.15 | 1.842 |

BIG 1 | -0.0002** | 0.565*** | 0.110*** | 0.350*** | -2.02 | 42.81 | 7.53 | 31.40 | 38.4% | 766.69 | 1.873 |

BIG | -0.0002 | 0.547*** | 0.426*** | 0.301*** | -1.63 | 35.56 | 25.01 | 23.14 | 32.8% | 601.56 | 1.947 |

Portfolios | αi | βMRP | βHML | βSMB | t(αi) | t(βMRP) | t(βHML) | t(βSMB) | Adjusted R2 | F-Ratio | D-W stat |

|---|---|---|---|---|---|---|---|---|---|---|---|

HIGH | -0.0003*** | 0.703*** | 0.524*** | 0.166*** | -3.16 | 56.44 | 38.01 | 15.80 | 52.3% | 1349.49 | 1.907 |

HIGH 1 | -0.0003*** | 0.538*** | 0.485*** | 0.038*** | -2.80 | 43.48 | 35.35 | 3.68 | 43.4% | 944.63 | 1.961 |

HIGH 2 | -0.0002 | 0.473*** | 0.043*** | 0.040*** | -1.34 | 36.41 | 3.01 | 3.60 | 26.9% | 453.84 | 1.987 |

LOW 2 | -0.0001 | 0.532*** | 0.038*** | 0.024** | -1.28 | 42.66 | 2.78 | 2.25 | 34.0% | 634.10 | 1.798 |

LOW 1 | -0.0003*** | 0.656*** | -0.365*** | 0.068*** | -2.86 | 53.96 | -27.11 | 6.61 | 53.4% | 1410.45 | 1.983 |

LOW | -0.0003** | 0.577*** | -0.564*** | 0.134*** | -2.21 | 42.83 | -37.81 | 11.78 | 51.6% | 1310.09 | 1.862 |

ASE | Amman Stock Exchange |

CAPM | Capital Asset Pricing Model |

FF3F | Fama and French Three-factor Model |

SMB | Small Minus Big (Size Risk Premium) |

HML | High Minus Low (Value Risk Premium) |

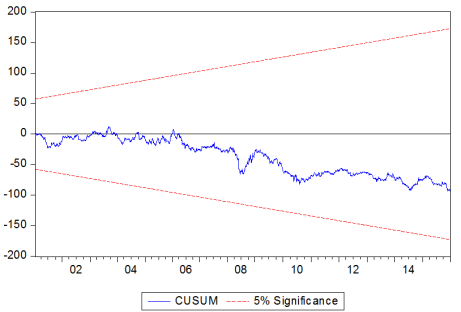

CUSUM | Cumulative Sum Test |

ADF | Augmented Dickey-fuller Test |

| [1] | Abbas, N., Khan, J., Aziz, R., & Sumrani, Z. (2014). A paper to check the applicability of Fama and French three-factor model on KSE 100-Index (2004–2014). International Journal of Financial Research, 6(1), 90. |

| [2] |

Acerbi, C., & Simonetti, P. (2002). Portfolio optimization with spectral measures of risk. arXiv preprint cond-mat/0203607. Retrieved from

http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.311.9257&rep=rep1&type=pdf |

| [3] | Ajlouni, M. M., Alrabadi, D. W., & Alnader, T. K. (2013). Forecasting the ability of dynamic versus static CAPM: Evidence from Amman Stock Exchange. Jordan Journal of Business Administration, 9(2), 431–443. |

| [4] | Ajlouni, M. M., & Khasawneh, M. (2017). Empirical test of Fama and French three-factor model in Amman Stock Exchange. Proceedings of the 6th Eurasian Multidisciplinary Forum (EMF 2017), Vienna, Austria, April 27–28. |

| [5] | Al-Mwalla, M. (2012). Can book-to-market, size, and momentum be extra risk factors that explain the stocks’ rate of return? Evidence from an emerging market. Journal of Finance, Accounting and Management, 3(2), 42–57. |

| [6] | Al-Mwalla, M., & Karasneh, M. (2011). Fama and French three-factor model: Evidence from an emerging market. European Journal of Economics, Finance and Administrative Sciences, 41, 132–140. |

| [7] | Ángel Martín Mato, M. (2005). Classic and modern measures of risk in fixed-income portfolio optimization. The Journal of Risk Finance, 6(5), 416–423. |

| [8] | Berger, T., & Fieberg, C. (2016). On portfolio optimization: Forecasting asset covariances and variances based on multi-scale risk models. The Journal of Risk Finance, 17(3), 295–309. |

| [9] | Blanco, B. (2012). The use of CAPM and Fama and French three-factor model in portfolio selection. Public and Municipal Finance, 1(2), 62–63. |

| [10] | Buraschi, A., Porchia, P., & Trojani, F. (2010). Correlation risk and optimal portfolio choice. The Journal of Finance, 65(1), 393–420. |

| [11] | Chan, L., Karceski, J., & Lakonishok, J. (1999). On portfolio optimization: Forecasting covariances and choosing the risk model. Review of Financial Studies, 12(5), 937–974. |

| [12] | Chau Li, W., Wu, Y., & Ojiako, U. (2014). Using portfolio optimization models to enhance decision-making and prediction. Journal of Modelling in Management, 9(1), 36–57. |

| [13] | Da, Z., & Schaumburg, E. (2011). The pricing of volatility risks across asset classes. University of Notre Dame and Federal Reserve Bank of New York (Working Paper). |

| [14] | Da, Z. (2009). Cash flow, consumption risk, and the cross-section of stock returns. The Journal of Finance, 7(2), 923–956. |

| [15] | Engles, M. (2004). Portfolio optimization: Beyond Markowitz (master’s thesis). Leiden University. |

| [16] | Eraslan, V. (2013). Fama and French three-factor model: Evidence from Istanbul Stock Exchange. Business and Economics Research Journal, 4(2), 11–22. |

| [17] | Fabozzi, F., Gupta, F., & Markowitz, H. (2002). The legacy of modern portfolio theory. The Journal of Investing, 11(3), 7–22. |

| [18] | Fama, E. F., & French, K. R. (1992). The cross-section of expected stock returns. Journal of Finance, 47(2), 427–465. |

| [19] | Fama, E. F., & French, K. R. (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33(1), 3–56. |

| [20] | Fama, E. F., & French, K. R. (1996). Multifactor explanations of asset pricing anomalies. The Journal of Finance, 51(1), 55–84. |

| [21] | Fama, E. F., & French, K. R. (2014). A five-factor asset pricing model. Journal of Financial Economics, 116(1), 1–22. |

| [22] | Fama, E. F., & MacBeth, J. D. (1974). Tests of the multiperiod two-parameter model. Journal of Financial Economics, 1(1), 43–66. |

| [23] | Gençay, R., Whitcher, B., & Selçuk, F. (2003). Systematic risk and time scales. Quantitative Finance, 3(2), 108–116. |

| [24] | Haugen, A. S. (2001). Modern investment theory (5th ed.). Prentice-Hall. |

| [25] | Ismal, R. (2014). An optimal risk–return portfolio of Islamic banks. Humanomics, 30(4), 286–303. |

| [26] | Kaplan, P. D. (1998). Asset allocation models using the Markowitz approach. In Frontiers of Modern Asset Allocation (pp. 267–274). |

| [27] | Karolyi, G. A., & Wu, Y. (2012). The role of investing ability restrictions on size, value, and momentum in international stock returns. Johnson School Research Paper Series (12-2012). |

| [28] | Kim, S., & In, F. (2007). A note on the relationship between Fama-French risk factors and innovations of ICAPM state variables. Finance Research Letters, 4(3), 165–171. |

| [29] | Krokhmal, P., Palmquist, J., & Uryasev, S. (2002). Portfolio optimization with conditional value-at-risk objective and constraints. Journal of Risk, 4, 43–68. |

| [30] | Li, S., Luong, C., Angkola, F., & Wu, Y. H. (2016). Optimal asset portfolio with stochastic volatility under the mean-variance utility with state-dependent risk aversion. Journal of Industrial and Management Optimization, 12(4), 1521–1533. |

| [31] | Lintner, J. (1965). The valuation of risk assets and the selection of risky investments in stock portfolios and capital budgets. The Review of Economics and Statistics, 47(1), 13–37. |

| [32] | Markowitz, H. (1959). Portfolio selection: Efficient diversification of investments. Basil Blackwell. |

| [33] | Markowitz, H. M. (1952). Portfolio selection. The Journal of Finance, 7(1), 77–91. |

| [34] | Miller, M. H., & Scholes, M. (1972). Rates of return in relation to risk: A reexamination of some recent findings. In Studies in the Theory of Capital Markets (Vol. 23, pp. 47–78). |

| [35] | Mossin, J. (1966). Equilibrium in a capital asset market. Econometrica, 98(2), 768–783. |

| [36] | Patton, A. J., & Timmermann, A. (2010). Monotonicity in asset returns: New tests with applications to the term structure, CAPM, and portfolio sorts. Journal of Financial Economics, 98(3), 605–625. |

| [37] | Ross, S. A. (1976). The arbitrage theory of capital asset pricing. Journal of Economic Theory, 13(3), 341–360. |

| [38] | Rotela Junior, P., Pamplona, E. D. O., Rocha, L. C. S., Valerio, V. E. D. M., & Pavia, A. P. (2015). Stochastic portfolio optimization using efficiency evaluation. Management Decision, 53(8), 1698–1713. |

| [39] | Sharpe, W. F. (1964). Capital asset prices: A theory of market equilibrium under conditions of risk. The Journal of Finance, 19(3), 425–442. |

| [40] | Sun, Y., Aw, G., Teo, K. L., & Zhou, G. (2015). Portfolio optimization using a new probabilistic risk measure. Journal of Industrial and Management Optimization, 11(4), 1275–1283. |

| [41] | Treynor, J. L. (1961). Market value, time, and risk. Unpublished manuscript. London: Risk Books. |

| [42] | Treynor, J. L. (1962). Toward a theory of market value of risky assets. Unpublished manuscript. London: Risk Books. |

| [43] | Trimech, A., Kortas, H., Benammou, S., & Benammou, S. (2009). Multiscale Fama–French model: Application to the French market. The Journal of Risk Finance, 10(2), 179–192. |

| [44] | Amman Stock Exchange (ASE). (n.d.). Amman Stock Exchange (official website). Retrieved February 20, 2026, from |

| [45] | Central Bank of Jordan (CBJ). (n.d.). Central Bank of Jordan (official website). Retrieved February 20, 2026, from |

APA Style

Hallaq, S. S. A., Ajlouni, M., Alfoul, L. A. (2026). Forecasting Asset Covariances and Variances Using Multi-scale Risk Models: Evidence from the Amman Stock Exchange. Journal of Business and Economic Development, 11(1), 1-15. https://doi.org/10.11648/j.jbed.20261101.11

ACS Style

Hallaq, S. S. A.; Ajlouni, M.; Alfoul, L. A. Forecasting Asset Covariances and Variances Using Multi-scale Risk Models: Evidence from the Amman Stock Exchange. J. Bus. Econ. Dev. 2026, 11(1), 1-15. doi: 10.11648/j.jbed.20261101.11

@article{10.11648/j.jbed.20261101.11,

author = {Said Sami Al Hallaq and Mohammad Ajlouni and Laith Abu- Alfoul},

title = {Forecasting Asset Covariances and Variances Using

Multi-scale Risk Models: Evidence from the Amman Stock Exchange},

journal = {Journal of Business and Economic Development},

volume = {11},

number = {1},

pages = {1-15},

doi = {10.11648/j.jbed.20261101.11},

url = {https://doi.org/10.11648/j.jbed.20261101.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.jbed.20261101.11},

abstract = {This study aims to forecast asset variances and covariances through the application of multi-scale risk models. Using daily data for 61 firms listed on the Amman Stock Exchange (ASE) over the period from January 1, 2001, to December 31, 2015, the analysis investigates the dynamic behaviour of asset returns across different time horizons. To enhance the robustness and reliability of the findings, several econometric and statistical techniques are employed, including the CUSUM test to assess structural stability, the Granger causality test to examine predictive relationships, wavelet transformation to capture time-frequency dynamics, and unit root tests to verify stationarity properties. The multi-scale risk model serves as the principal analytical framework, allowing for a comprehensive examination of the evolving interdependencies among asset returns. The empirical results indicate that market risk premium coefficients significantly explain variations in portfolio returns, highlighting the importance of systematic risk factors in asset pricing. Furthermore, portfolios composed of lower-value stocks outperform those containing higher-value stocks, while smaller-sized portfolios consistently generate higher returns than larger-sized portfolios during the sample period. Overall, the findings demonstrate the effectiveness of multi-scale risk models in forecasting asset variances and covariances. The model exhibits strong explanatory power in capturing daily portfolio return dynamics on the ASE, thereby contributing to improved portfolio optimization strategies and more accurate risk prediction. These results underscore the practical and theoretical value of multi-scale modelling in financial risk management.},

year = {2026}

}

TY - JOUR T1 - Forecasting Asset Covariances and Variances Using Multi-scale Risk Models: Evidence from the Amman Stock Exchange AU - Said Sami Al Hallaq AU - Mohammad Ajlouni AU - Laith Abu- Alfoul Y1 - 2026/02/28 PY - 2026 N1 - https://doi.org/10.11648/j.jbed.20261101.11 DO - 10.11648/j.jbed.20261101.11 T2 - Journal of Business and Economic Development JF - Journal of Business and Economic Development JO - Journal of Business and Economic Development SP - 1 EP - 15 PB - Science Publishing Group SN - 2637-3874 UR - https://doi.org/10.11648/j.jbed.20261101.11 AB - This study aims to forecast asset variances and covariances through the application of multi-scale risk models. Using daily data for 61 firms listed on the Amman Stock Exchange (ASE) over the period from January 1, 2001, to December 31, 2015, the analysis investigates the dynamic behaviour of asset returns across different time horizons. To enhance the robustness and reliability of the findings, several econometric and statistical techniques are employed, including the CUSUM test to assess structural stability, the Granger causality test to examine predictive relationships, wavelet transformation to capture time-frequency dynamics, and unit root tests to verify stationarity properties. The multi-scale risk model serves as the principal analytical framework, allowing for a comprehensive examination of the evolving interdependencies among asset returns. The empirical results indicate that market risk premium coefficients significantly explain variations in portfolio returns, highlighting the importance of systematic risk factors in asset pricing. Furthermore, portfolios composed of lower-value stocks outperform those containing higher-value stocks, while smaller-sized portfolios consistently generate higher returns than larger-sized portfolios during the sample period. Overall, the findings demonstrate the effectiveness of multi-scale risk models in forecasting asset variances and covariances. The model exhibits strong explanatory power in capturing daily portfolio return dynamics on the ASE, thereby contributing to improved portfolio optimization strategies and more accurate risk prediction. These results underscore the practical and theoretical value of multi-scale modelling in financial risk management. VL - 11 IS - 1 ER -

Department of Business Economics, Yarmouk University, Irbid, Hashemite Kingdom of Jordan

Cairo Amman Bank, Amman, Hashemite Kingdom of Jordan