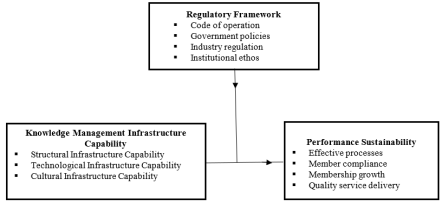

Deposit-Taking Savings and Credit Cooperative Societies (DT-SACCOs) are essential drivers of economic development through enhancing financial inclusion and fostering economic growth within communities. Despite their importance, DT-SACCOs in Kenya are facing declining performance. This study investigated whether the regulatory framework moderates the relationship between knowledge management infrastructure capability and the organizational performance of DT-SACCOs in Kenya. In this study, knowledge management infrastructure capability is recognized as a strategic tool that is designed to make organizational performance better. Given that DT-SACCOs operate within a heavily regulated environment, it is hypothesized that regulatory framework influences how investments in knowledge management infrastructure capability translate into organizational performance improvements. Anchored in the resource-based view theory, knowledge-based view theory and the balanced scorecard model with support from open systems theory to explain the moderating influence of regulation, this study adopted descriptive and explanatory research designs under a positivism philosophy. The research targeted 176 DT-SACCOs in Kenya, focusing on 880 managers across finance, human resources, ICT, legal and marketing at their headquarters. Using stratified proportional sampling, 275 respondents from 55 randomly selected DT-SACCOs participated in the study. Data was collected via a semi-structured questionnaire, with reliability confirmed through Cronbach’s Alpha coefficients exceeding 0.7. Validity was ensured through face, content, and construct assessments. Descriptive statistics outlined the characteristics of study variables, while multiple regression analysis examined the relationships among knowledge management infrastructure capability, organizational performance, and the moderating role of the regulatory framework. Findings revealed that KMIC significantly enhances organizational performance in DT-SACCOs and that the regulatory framework positively moderates this relationship. The study advises DT-SACCOs to prioritize recruiting skilled managers, fostering transparent and accessible service environments, and focusing employee training on quality service delivery. Additionally, it recommends that DT-SACCOs maintain flexibility in managing resources to effectively capitalize on emerging business opportunities.

| Published in | Journal of Business and Economic Development (Volume 11, Issue 1) |

| DOI | 10.11648/j.jbed.20261101.12 |

| Page(s) | 16-30 |

| Creative Commons |

This is an Open Access article, distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution and reproduction in any medium or format, provided the original work is properly cited. |

| Copyright |

Copyright © The Author(s), 2026. Published by Science Publishing Group |

Knowledge Management Infrastructure Capability, Organizational Performance, Regulatory Framework, Deposit-Taking Savings, Credit Cooperative Societies in Kenya

Research Variable | Cronbach's Alpha | Decision |

|---|---|---|

Structural infrastructure capability | 0.791 | Reliable |

Technological infrastructure capability | 0.776 | Reliable |

Cultural infrastructure capability | 0.747 | Reliable |

Regulatory framework | 0.843 | Reliable |

Organizational Performance | 0.738 | Reliable |

Aggregate Score | 0.779 | Reliable |

Variable | Mean | Standard deviation |

|---|---|---|

Structural infrastructure capability | 4.11 | 0.68 |

Technological infrastructure capability | 3.88 | 0.79 |

Cultural infrastructure capability | 4.05 | 0.72 |

Aggregate mean for green innovation strategy | 4.01 | 0.73 |

Variable (Regulatory framework | Mean | Standard deviation |

|---|---|---|

The regulatory framework is prohibitive to DT-SACCOs business | 2.64 | 0.92 |

DT-SACCOs in our country face stringent rules and regulations by the Government of Kenya | 3.14 | 1.10 |

Industry regulation set by the industry players are very demanding by DT-SACCOs | 3.14 | 1.08 |

Professional standards established by industry stakeholders are highly rigorous and comprehensive | 3.08 | 1.10 |

The existing code of operations in our DT-SACCO is comprehensive enough for task performance | 3.79 | 0.72 |

Our DT-SACCO adheres to all the established regulatory framework | 4.23 | 0.65 |

Pressure to conform to standard industry practices constrains DT-SACCOs’ innovativeness | 3.22 | 1.01 |

Aggregate mean for regulatory framework | 3.32 | 0.93 |

Variable | Mean | Standard deviation |

|---|---|---|

Our flexible processes enhance the uptake of DT- SACCO products and services | 4.08 | 0.54 |

Our members associate us with delivery of higher quality service | 4.01 | 0.68 |

Our systems are built to enable members’ convenience | 4.16 | 0.73 |

Our DT-SACCO makes effort to attract new members | 4.41 | 0.64 |

Our employees are actively involved in remittance follow up in order to improve members compliance | 3.98 | 0.71 |

Employees are well trained to ensure customer consistency in remitting their statutory contributions | 4.10 | 0.79 |

We encourage prompt customer feedback. | 4.15 | 0.87 |

Our members’ high retention rate is due to loyalty to our DT-SACCO | 3.98 | 0.85 |

Aggregate mean for organizational performance | 4.11 | 0.75 |

Model Summaryb | |||||||

|---|---|---|---|---|---|---|---|

Model | R | R Square | Adjusted R Square | Std. Error of the Estimate | |||

1 | .724a | 0.525 | 0.466 | 0.39027 | |||

ANOVAa | |||||||

Model | Sum of Squares | df | Mean Square | F | Sig. | ||

Regression | 17.471 | 3 | 5.824 | 29.585 | .000b | ||

Residual | 37.008 | 188 | 0.197 | ||||

Total | 54.479 | 191 | |||||

Coefficientsa | |||||||

Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | |||

β | Std. Error | Beta | |||||

1 | (Constant) | 1.204 | 0.489 | 2.464 | 0.015 | ||

Knowledge Management Infrastructure Capability | 0.718 | 0.100 | 0.461 | 7.168 | 0.000 | ||

a. Dependent Variable: Organizational Performance | |||||||

Model Summary | ||||||

|---|---|---|---|---|---|---|

Model | R | R Square | Adjusted R Square | Std. Error of the Estimate | ||

1 | .499a | 0.249 | 0.241 | 0.46541 | ||

a. Predictors: (Constant), Interaction term, Knowledge Management Infrastructure Capability and Regulatory Framework | ||||||

ANOVAa | ||||||

Model | Sum of Squares | df | Mean Square | F | Sig. | |

1 | Regression | 13.541 | 2 | 6.770 | 31.257 | .000b |

Residual | 40.938 | 189 | 0.217 | |||

Total | 54.479 | 191 | ||||

a. Dependent Variable: Performance | ||||||

b. Predictors: (Constant), Interaction term, Knowledge Management Infrastructure Capability and Regulatory Framework | ||||||

Coefficientsa | ||||||

Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | ||

β | Std. Error | Beta | ||||

1 | (Constant) | 1.557 | 0.493 | 3.159 | 0.002 | |

Knowledge Management Infrastructure Capability | 0.464 | 0.130 | 0.298 | 3.580 | 0.000 | |

Regulatory Framework | 0.323 | 0.114 | 0.118 | 2.836 | 0.001 | |

Interaction terms of predictors and moderation variable | 0.040 | 0.013 | 0.250 | 2.996 | 0.003 | |

a. Dependent Variable: Organizational Performance | ||||||

DT-SACCOs | Deposit Taking Savings and Credit Cooperative Societies |

GDP | Gross Domestic Product |

ICT | Information and Communications Technology |

NGOs | Non-Governmental Organizations |

RBV | Resource Based View |

SACCO | Savings and Credit Cooperative Society |

SASRA | Sacco Societies Regulatory Authority |

| [1] | Abdel, M. H. (2012). Economic impacts of microfinance in developing markets. Journal of Development Economics, 45(2), 123-145. |

| [2] |

Ahmed, M. A. & Waithaka, P. (2018). Implementation of Strategic Plans and Performance of SACCOs in Nyeri County, Kenya, The International Journal of Business & Management, 6(12), 19-29.

https://doi.org/10.24940/theijbm/2018/v6/i12/139360-394435-1-SM |

| [3] |

Akram, M. (2018). Factors affecting foreign direct investment: Evidence from Pakistan. Journal of Economics and Sustainable Development, 9(4), 1-12.

https://www.iiste.org/Journals/index.php/JEDS/article/view/41300 |

| [4] |

Ali, H. (2021). Regulatory Framework and Microfinance Institutions’ Performance within the West African Monetary Union, AERC Research Paper 434 African Economic Research Consortium, Nairobi.

https://ideas.repec.org/p/aer/wpaper/e7d05b8b-254b-44f2-b7ec-7f734c0f16ed.html |

| [5] | Aries, H. P., Wei, L. & Ariana, C. (2016). Network model for social entrepreneurships: Pathways to sustainable competitive advantage, Journal of Small Business and Entrepreneurship Development, 4(1), 44-53. |

| [6] | Armbretch, F., Chapas, R., Chappelow, C., Farris, G., Friga, P., Hartz, C., Mcllvaine, M., Postle, S., & Whitwell, G. (2001). Knowledge management in research and development, Knowledge Management Research Development, 44(4), 1-28. |

| [7] | Bastedo, M. N. (2004). Open Systems Theory, The SAGE Encyclopedia of Educational Leadership and Administration Draft: April 28, 2004. |

| [8] | Barney, J. (1991) Firm resources and sustained competitive advantage, Journal of Management, 17(1), 99-120. |

| [9] | Bertalanffy, L. V. (1950). An Outline of General System Theory, The British Journal for the Philosophy of Science, 1(2), 134-165. |

| [10] | Bertalanffy, L. V. (1956). General System Theory, Yearbook of the Society for the Advancement of General System Theory. |

| [11] | Chenhall, R. H., & Langfield-Smith, K. (2007). Multiple Perspectives of Performance Measures, European Management Journal, 25(4), 266-282. |

| [12] | Chiu, C., & Chen. H. (2016). The study of knowledge management capability and organizational effectiveness in Taiwanese Public Utility: the mediator role of organizational commitment, Springer Plus, 5(2016), 1-34. |

| [13] | Cooper, D. R. & Schindler, P. S. (2011). Business Research Methods, 9th Ed. New Delhi: Tata McGraw-Hill Education Private Limited. |

| [14] | Field, A. (2013). Discovering statistics using IBM SPSS statistics. California, United States: Sage publications. |

| [15] | Fraihat, B. A. & Samadi, B. (2017). Knowledge Management Capabilities and Organizational Performance of Public Listed Companies: A Conceptual Framework, International journal of Business and Social Research, 7(11), 9-20. |

| [16] | Fincham, J. E. (2008). Response rates and responsiveness for surveys, standards, and the Journal. American Journal of Pharmaceutical Education, 72(2), 43. |

| [17] | Gold, A. H., Malhotra, A., & Segars, A. H. (2001). Knowledge management: an organizational capabilities perspective, Journal of Management Information Systems, 18(1), 185-214. |

| [18] | Grant, R. M. (1996). Toward a knowledge-based theory of the firm. Strategic Management Journal, 17(S2), 109-122. |

| [19] | Hefu, L., Dandan, S. & Zhao, C. (2014). Knowledge Management Capability and Firm Performance: The Mediating Role of Organizational Agility. 18th Pacific Asia Conference on Information Systems, PACIS 2014, Chengdu, China, June 24-28, 2014. pages 165. |

| [20] | Helfat, C. E., Finkelstein, S., Mitchell, W., Peteraf, M., Singh, H., Teece, D. & Winter, S. G. (2007). Dynamic capabilities: Understanding strategic change in organizations. Malden, MA: Blackwell Publishing. |

| [21] | Isorite, M. (2008). The Balanced Scorecard Method: from theory to practice, Intellectual economics. 1(3), 18-28. |

| [22] | Joshua, C. & Kinyua, G. M. (2025). Knowledge Process Capability as an Antecedent of Firm Performance: Evidence from Review of Literature. International Journal of Education and research, 13(3): 1-34. |

| [23] | Kaplan, R. S. & Norton, P. (1996). The Balance Score Card: Translating strategy into Action. Harvard Business School Press, Boston MA. |

| [24] | Katz, D., Kahn, R. L. 1978. The Social Psychology of Organizations, II ed. New York: Wiley. |

| [25] | Kenya Financial Stability Report, 2021. (2022). Kenya Financial Sector Stability Report, Financial Sector Regulators, July 2022, Issue No. 13, 1-67. |

| [26] | Kabera, B. N. & Kinyua, G. M. (2024). Community of Practice as an Imperative for Organizational Performance in the Context of Non-Governmental Organizations in Kiambu County, Kenya. Journal International of Business Management, 5(1): 197-207. |

| [27] | Kela-Kahingo, C. M., Kinyua, G. M. & Muchemi, A. (2024). Strategic Flexibility as a Predictor of Organisation Performance in Commercial Banks in Kenya: The Mediating Role of Organisational Competences. International Journal of Education and Research, 12(10). 153-174. |

| [28] | Kiaritha, H. W., (2015). Determinants of the Financial Performance of Savings and Credit Co-operatives in the Banking Sector in Kenya. (Unpublished PhD Thesis), Jomo Kenyatta University of Agriculture and Technology. |

| [29] | Kinuu, D. (2014). Top management team psychological characteristics, institutional environment, team processes and performance of companies listed in Nairobi Securities Exchange [Doctoral dissertation, University of Nairobi]. University of Nairobi Digital Repository. |

| [30] | Kinyua, G. M. 2015. Relationship between Knowledge Management and Performance of Commercial Banks in Kenya. (Unpublished PhD), Kenyatta University. |

| [31] | Kori, B. W., Muathe, S. M., & Maina, S. M. (2020). Strategic Intelligence Practices and Performance of the Banking Industry: The Role of Regulatory Framework in Commercial Banks in Kenya. International Journal of Economics, Commerce and Management. 8(9), 246-265. |

| [32] | Kung’u, S. M., Kahuthia, J. & Kinyua, G. (2020). Analysis of the Effect of Strategic Direction on Performance of Motor Vehicle Assembly Firms in Nairobi City County, Kenya. International Journal of Managerial Studies and Research, 8(8), 82-94. |

| [33] | Kwanya, T. & Awino, J. (2019). Knowledge Sharing and Diffusion Strategies in Savings and Credit Cooperatives in Kenya, African Journal of Co-operative Development and Technology, 4(1), 1-10. |

| [34] | Kogut, B. & Zander, U. (1992). Knowledge of Enterprise, Combinative Capabilities and the Replication of Technology. Organizational Science, 3(3), 383-397. |

| [35] | Lai, Y.-H., & Lin, T.-B. (2012). The effects of learner motivation on learning outcomes in blended learning environments. Computers & Education, 58(4), 1023-1032. |

| [36] | Lebans, M., & Euske, K. (2006). A conceptual and operational delineation of performance, Business performance measurement, Cambridge University Press. |

| [37] | Mbulwa, J. & Kinyua, G. (2021). The Role of Strategy Formulation on Service Delivery: A Perspective of Turkana County in Kenya. International Journal of Innovative Research and Advanced Studies, 8(3): 16 - 23. |

| [38] | Mele, C., Pels, J., Polese, F. (2010). A Brief Review of Systems Theories and Their Managerial Applications, Journal of Service Science, 2(1-2), 126 - 135. |

| [39] | Mirie, M. 2014. The Influence of Members’ Income and Conduct of SACCS in the Relationship Between Characteristics and Efficiency of SACCOS in Kenya. (Unpublished Ph.D Thesis), University of Nairobi. |

| [40] | Mogaka, D. M., Kinyua, G. M. & Kimencu, L. (2025). The Nexus between Inter-Firm Networks and Firm Performance: Context-Specific Empirical Evidence of the Interceding Role of Competitive Advantage. The International Journal of Humanities & Social Studies, 13(7): 57 - 73. |

| [41] | Mogaka, D. M., Kinyua, G. & Kimencu, L. (2025). Does Regulatory Framework Moderate the Nexus Between Inter-Firm Networks and Firm Performance? Empirical Evidence from Pharmaceutical Manufacturing Firms in Nairobi City County, Kenya. International Journal of Economics, Commerce and Management, 13(8): 41-71. |

| [42] | Mubarak, K., & Sabraz, N. S. (2020). Impact of Knowledge Management Capabilities on Performance of Star Hotels in Sri Lanka, International journal of Advanced Science and Technology, 29(4), 1102-1112. |

| [43] | Muteshi, H. K., Maina, S. & Kinyua, G. (2022). Country Regulatory Environment, Moderating Country Brand Choice for Foreign Direct Investment in Kenya. Journal International of Business Management, 3(1), 66 - 89. |

| [44] | Muthimi, J. K., Kilika, J. M. & Kinyua, G. (2021). Exploring the role of inspirational motivation to institutions of higher learning: Empirical evidence from selected universities in Kenya. International Journal of Research in Business and Social Science, 10(4): 455-466. |

| [45] | Nada I. J., Rusinah, S., Ibrahim, Z., Mahmoud, K. (2016). Impact of Information Technology Infrastructure on Innovation Performance: An Empirical Study on Private Universities in Iraq, Procedia Economics and Finance, 39(2016), 861 - 869. |

| [46] | Ndiwa, E. C. & Kinyua, G. M. (2024). Learning Orientation and Firm Performances in the Context of Construction Firms in Nairobi County, Kenya. Journal of Business and Management, 26(11): 52-64. |

| [47] | Ndumia, S. N. (2015). Influence of regulatory framework on performance of building construction projects in Nairobi County, Kenya. Master’s Research Project, University of Nairobi, Unpublished. |

| [48] | Nisha, N. (2017). An Empirical Study of the Balanced Scorecard Model: Evidence from Bangladesh, International Journal of Information Systems in the Service Sector, 9(1), 68-84. |

| [49] | Nyankomo, M. (2015). Efficiency and Sustainability of Tanzanian saving and Credit Cooperatives. (Unpublished Ph.D Thesis), University of Stellenbosch. |

| [50] | Nzomo, J. K., Kinyua, G. M. & Mwasiaji, E. T. (2023). Green Innovation Strategy as Antecedent of Performance Sustainability among ISO 14001-Certified Manufacturing Firms in Kenya: Does Regulatory Framework Play a Moderating Role? The International Journal of Humanities & Social Studies, 11(8): 198-207. |

| [51] | Oketch, J. O., Kilika, J. M. & Kinyua, G. M. (2021). TMT Characteristics and Organizational Performance in a Regulatory Setting in Kenya. Journal of Economics and Business, 4(1): 79-92. |

| [52] | Oluoch F. O, K’Aol, G. and Koshal J. (2021). Moderating Influence of Regulatory Framework on the Relationship between Strategic Leadership and Financial Sustainability on NGO’s in Kenya, The University Journal, 3(2), 13-26. |

| [53] | Oliver, S. & Kandadi, K. R. (2006). How to develop knowledge culture in organizations? A multiple case study of large distributed organizations, Journal of Knowledge Management, 10(4), 6-24. |

| [54] | OuYang, Y. (2015). A Cyclic Model for Knowledge Management Capability-A Review Study, Arabian Journal of Business and Management Review, 5(2), 2-9. |

| [55] | Pearce J. & Robinson, R. (2005). Strategic Management: Strategy Formulation Implementation and Control. 10th Ed. Mchraw-Hill, New York. |

| [56] | Ra’ed, M., Amaithan, A. A., Ala’aldin, A. & Bader, O. (2019). The Role of Knowledge Management Infrastructure in Enhancing Job Satisfaction: ADeveloping Country Perspective, Interdisciplinary Journal of Information, Knowledge and Management, 14(2019), 1-25. |

| [57] | SACCO Supervision Annual Report, 2021. (2022). The Annual Statutory Report on the operations and performance of SACCO Societies in Kenya, The SACCO Societies Regulatory Authority, 1-135. |

| [58] | SACCO supervision annual report, 2022. (2023). The Annual Statutory Report on the operations and performance of Regulated SACCO Societies in Kenya, The SACCO Societies Regulatory Authority, 1-167. |

| [59] | Samad, S. (2020). Achieving innovative firm performance through human capital and the effect of social capital. Management & Marketing, 15(2), 326-344. |

| [60] | Sambamurthy, V., Wei, K., Lim, K., & Lee, D. (2007). IT-Enabled Organizational Agility and Firms' Sustainable Competitive Advantage, ICIS 2007 Proceedings. Paper 91. |

| [61] | Sangeeta, S. B., Sumedha, C., & Aparna, R. (2015). Impact of Knowledge Management Capabilities on Knowledge Management Effectiveness in Indian Organizations, The Journal for Decision Makers, 40(4), 421-434. |

| [62] | Satwinder, S., Tamer, K D. & Kristina, P. 2016. Measuring Organizational Performance: A Case for Subjective Measures, British Journal of Management, 27(1), 214-224. |

| [63] | Saunders, M. N. (2011). Research methods for business students, 5thEd. Pearson Education India. |

| [64] | Saunders, M., Lewis, P. & Thornhill, A. (2007). Research Methods for Business Students. 4th Ed. Prentice Hall: Harlow, UK. |

| [65] | Saunders, M., Lewis, P. & Thornhill, A. (2009). Research Methods for Business Students. 5th Ed. London: Prentice Hall. |

| [66] | Sivagiri, N. (2018). The Effects of Knowledge Management Infrastructure Capability on Knowledge Management Effectiveness of Doctors: An Empirical Study, Journal of Management, 5(5), 218-231. |

| [67] | Shurie, F. B. O., Kilika, J. M., & Muchemi, A. W., (2022). Restructuring Strategies and Performance of Small and Medium Commercial Banks in Nairobi City County, Kenya. (Doctoral Thesis, School of Business, Kenyatta University). |

| [68] | Sin, L. Y. M., & Tse, A. C. B. (2000). Profiling Asian business-to-business relationships: An empirical investigation. Journal of Business-to-Business Marketing, 7(2-3), 57-89. |

| [69] | Somnuk, A., Pakchong, V., Achara, C., & Pracob, C. (2010). Indicators of knowledge management capability for KM effectiveness, The Journal of Information and Knowledge Management Systems, 40(2), 183-203. |

| [70] | Stewart, A. C. and Julie, C. H. (2001). The Balanced Scorecard: Beyond Reports and Rankings, Planning for Higher Education, 37-42. |

| [71] | Tavakol, M., & Dennick, R. (2011). Making sense of Cronbach's alpha. International journal of medical education, 2, 53. |

| [72] | Teece, D. J., Pisano, G. & Shuen, A. (1997). Dynamic capabilities and strategic management. Strategic Management Journal, 18(7): 509-533. |

| [73] | Tomal, D. R. and Jones, K. J. (2015) A Comparison of Core Competencies of Women and Men Leaders in the Manufacturing Industry. The Coastal Business Journal, 14, 13-25. |

| [74] | Tsetim, J. T., Ochanya B. A., and Agema, J. M. (2020). Knowledge Management Infrastructure Capabilities and Innovativeness of Small and Medium Scale Enterprises in Benue State, Nigeria, Saudi Journal of Business and Management Studies, 5(3), 216-225. |

| [75] | Vianney, U. J. M., Iravo, M., and Namusonge, G. (2020). Moderating Influence of Legal Framework on Board Leadership Practices and Corporate Governance Performance in Public Institutions in Rwanda, American Journal of Leadership and Governance, 5(1), 1-9. |

| [76] | Wandiga, W. (2019). Operations Strategy and Performance Management of Consultancy Firms in Nairobi City County, (Unpublished PhD Thesis), Kenyatta University. |

| [77] | Wernerfelt, B. (1984). A Resource-Based View of the Firm. Strategic Management Journal, 5(2): 171-180. |

| [78] | William, J., Smith, A., & Johnson, K. (2011). Strategic marketing in emerging markets: A comparative analysis. Journal of Financial Services Marketing, 16(3), 245-262. |

| [79] | World Council of Credit Union. (2020). World Council Annual Report 2020, The Global Network of Credit Unions and Financial Cooperatives. |

| [80] | Zhao, J. (2019). The Knowledge-based view Framework: Capability of Knowledge Integration Leads to Capability of Innovation or Imitation, International Journal of Economics, Commerce and Management, 7(10), 240-268. |

APA Style

Obonyo, M. O., Kinyua, G. M., Muchemi, A. W. (2026). Harnessing Knowledge Management Infrastructure Capability for Valuable Organizational Results: The Moderating Role of Regulatory Framework. Journal of Business and Economic Development, 11(1), 16-30. https://doi.org/10.11648/j.jbed.20261101.12

ACS Style

Obonyo, M. O.; Kinyua, G. M.; Muchemi, A. W. Harnessing Knowledge Management Infrastructure Capability for Valuable Organizational Results: The Moderating Role of Regulatory Framework. J. Bus. Econ. Dev. 2026, 11(1), 16-30. doi: 10.11648/j.jbed.20261101.12

@article{10.11648/j.jbed.20261101.12,

author = {Moses Ochieng Obonyo and Godfrey Mungai Kinyua and Ann Wambui Muchemi},

title = {Harnessing Knowledge Management Infrastructure Capability for Valuable Organizational Results:

The Moderating Role of Regulatory Framework},

journal = {Journal of Business and Economic Development},

volume = {11},

number = {1},

pages = {16-30},

doi = {10.11648/j.jbed.20261101.12},

url = {https://doi.org/10.11648/j.jbed.20261101.12},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.jbed.20261101.12},

abstract = {Deposit-Taking Savings and Credit Cooperative Societies (DT-SACCOs) are essential drivers of economic development through enhancing financial inclusion and fostering economic growth within communities. Despite their importance, DT-SACCOs in Kenya are facing declining performance. This study investigated whether the regulatory framework moderates the relationship between knowledge management infrastructure capability and the organizational performance of DT-SACCOs in Kenya. In this study, knowledge management infrastructure capability is recognized as a strategic tool that is designed to make organizational performance better. Given that DT-SACCOs operate within a heavily regulated environment, it is hypothesized that regulatory framework influences how investments in knowledge management infrastructure capability translate into organizational performance improvements. Anchored in the resource-based view theory, knowledge-based view theory and the balanced scorecard model with support from open systems theory to explain the moderating influence of regulation, this study adopted descriptive and explanatory research designs under a positivism philosophy. The research targeted 176 DT-SACCOs in Kenya, focusing on 880 managers across finance, human resources, ICT, legal and marketing at their headquarters. Using stratified proportional sampling, 275 respondents from 55 randomly selected DT-SACCOs participated in the study. Data was collected via a semi-structured questionnaire, with reliability confirmed through Cronbach’s Alpha coefficients exceeding 0.7. Validity was ensured through face, content, and construct assessments. Descriptive statistics outlined the characteristics of study variables, while multiple regression analysis examined the relationships among knowledge management infrastructure capability, organizational performance, and the moderating role of the regulatory framework. Findings revealed that KMIC significantly enhances organizational performance in DT-SACCOs and that the regulatory framework positively moderates this relationship. The study advises DT-SACCOs to prioritize recruiting skilled managers, fostering transparent and accessible service environments, and focusing employee training on quality service delivery. Additionally, it recommends that DT-SACCOs maintain flexibility in managing resources to effectively capitalize on emerging business opportunities.},

year = {2026}

}

TY - JOUR T1 - Harnessing Knowledge Management Infrastructure Capability for Valuable Organizational Results: The Moderating Role of Regulatory Framework AU - Moses Ochieng Obonyo AU - Godfrey Mungai Kinyua AU - Ann Wambui Muchemi Y1 - 2026/02/28 PY - 2026 N1 - https://doi.org/10.11648/j.jbed.20261101.12 DO - 10.11648/j.jbed.20261101.12 T2 - Journal of Business and Economic Development JF - Journal of Business and Economic Development JO - Journal of Business and Economic Development SP - 16 EP - 30 PB - Science Publishing Group SN - 2637-3874 UR - https://doi.org/10.11648/j.jbed.20261101.12 AB - Deposit-Taking Savings and Credit Cooperative Societies (DT-SACCOs) are essential drivers of economic development through enhancing financial inclusion and fostering economic growth within communities. Despite their importance, DT-SACCOs in Kenya are facing declining performance. This study investigated whether the regulatory framework moderates the relationship between knowledge management infrastructure capability and the organizational performance of DT-SACCOs in Kenya. In this study, knowledge management infrastructure capability is recognized as a strategic tool that is designed to make organizational performance better. Given that DT-SACCOs operate within a heavily regulated environment, it is hypothesized that regulatory framework influences how investments in knowledge management infrastructure capability translate into organizational performance improvements. Anchored in the resource-based view theory, knowledge-based view theory and the balanced scorecard model with support from open systems theory to explain the moderating influence of regulation, this study adopted descriptive and explanatory research designs under a positivism philosophy. The research targeted 176 DT-SACCOs in Kenya, focusing on 880 managers across finance, human resources, ICT, legal and marketing at their headquarters. Using stratified proportional sampling, 275 respondents from 55 randomly selected DT-SACCOs participated in the study. Data was collected via a semi-structured questionnaire, with reliability confirmed through Cronbach’s Alpha coefficients exceeding 0.7. Validity was ensured through face, content, and construct assessments. Descriptive statistics outlined the characteristics of study variables, while multiple regression analysis examined the relationships among knowledge management infrastructure capability, organizational performance, and the moderating role of the regulatory framework. Findings revealed that KMIC significantly enhances organizational performance in DT-SACCOs and that the regulatory framework positively moderates this relationship. The study advises DT-SACCOs to prioritize recruiting skilled managers, fostering transparent and accessible service environments, and focusing employee training on quality service delivery. Additionally, it recommends that DT-SACCOs maintain flexibility in managing resources to effectively capitalize on emerging business opportunities. VL - 11 IS - 1 ER -

Department of Business Administration, Kenyatta University, Nairobi, Kenya

Department of Business Administration, Kenyatta University, Nairobi, Kenya

Department of Business Administration, Kenyatta University, Nairobi, Kenya